Hello Sovryn‘s,

this post is about the XUSD lending pool. It aims to provide data and analysis. In addition, there will be a related proposal to cut the XUSD lending pool liquidity mining rewards.

Using the Sovryn subgraph, we performed an analysis of the XUSD lending pool. Every 20,000 blocks (about 1 week) we queried the blockchain data to get an overview of the last year. We would like to present the results in the following.

The data presented here show slight inaccuracies. However, this does not distort the overall picture.

First, let’s take a look at some lending volumes and the revenue generated by lending and borrowing:

Lending and borrowing generates some revenue. There is constant demand for borrowing XUSD, but the growth is quite stagnant for some time now. In total, stakers received about 200.000 USD worth of revenue from borrowing and lending fees until now.

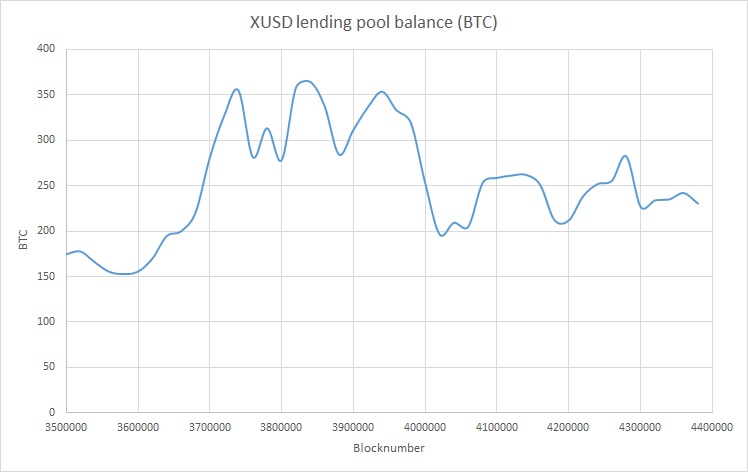

In addition, here’s the XUSD lending pool balance:

Because there are LM incentives in SOV in addition to the XUSD APY, i would like to show the SOV price as comparison. It appears that the SOV price has influence on the XUSD lending pool balance. In addition, here’s the lending pool balance measured in BTC:

Interestingly, when measured in BTC, the lending pool balance is forming higher lows and still sits well above 200 btc as it did for most of the time. It may be the case that user’s borrow XUSD against their btc and put it into the XUSD lending pool to farm SOV rewards. Usually, doing this would not be profitable because borrowing interest is always higher than lending interest. But the $SOV rewards make this strategy profitable. The platform generates revenue with this strategy, but it also has a cost. And this cost is very high. How high, is shown below.

The lending pool is running on a huge loss for a year now. 15,000 SOV are paid as rewards to XUSD liquidity providers per week. This cost is shown here in BTC, calculated for each block interval using the price at that time. For comparison, this chart also shows the staker revenue for the respective block intervals and the resulting loss. In case anyone is wondering why LM costs are dropping so much, this is due to the falling SOV price.

If we take a look at the XUSD pool balance and compare it with the SOV price, you can see a correlation. As the SOV price falls, the pool balance also falls. The SOV-based portion of the APY falls, making the pool less attractive.

The pool also pays out APY in XUSD, and this is not bad at all. But just not at degen-defi level.

Would liquidity providers also be inclined to deposit XUSD if there were less SOV rewards? The next chart suggests this.

If the lending pool balance was mainly dependent on the SOV liquidity mining rewards and the SOV price, I would expect the pool balance to be constant in relation to the SOV token price. However, it is increasing rapidly. This shows that the XUSD-based APY is sufficient to attract liquidity.

Stay Sovryn!